Understanding four key motivations for sustainable investing

Your investments make an impact on the world – whether deliberately or not. The question is: is that the impact you, your family or your organisation, want to make?

As private wealth holders, your investments can address social and environmental challenges in ways that complement government action and philanthropy. Sustainable investing offers a range of approaches to invest intentionally to generate financial returns and societal impact aiming to protect and grow your assets, while making a positive contribution to our world.

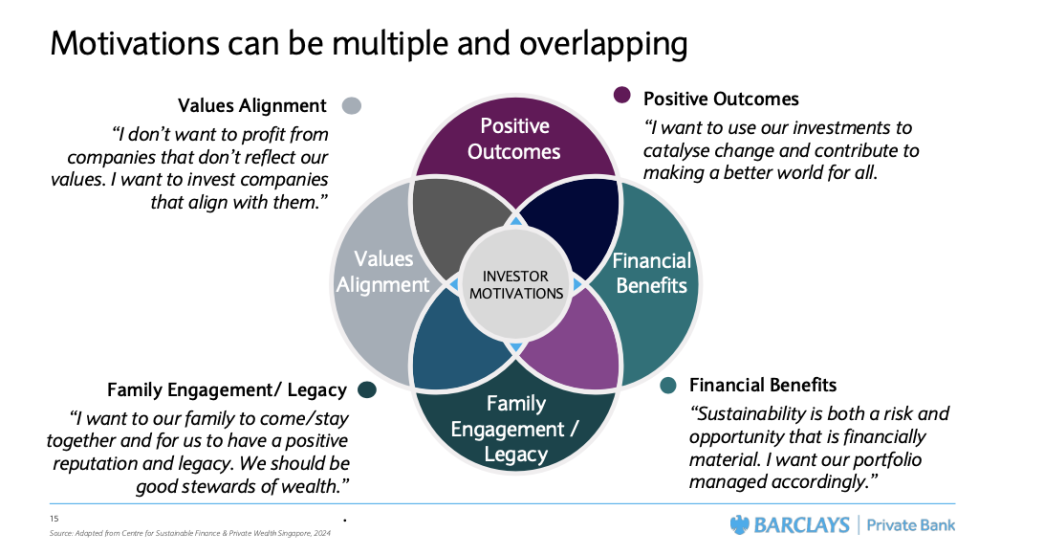

At the Center for Sustainable Finance and Private Wealth (CSP), over ten years of dialogue and education programmes, we consistently found four key motivations that drive wealth holders to sustainable investing. (see Figure 1)

Figure 1: Four key motivations to invest sustainably

Understanding these motivations can transform how you approach your portfolio, family dynamics and wealth. In this first article, we explore:

- What are these four motivations and why might each occur?

- What outcomes does each motivation seek? And what investment strategies can be used to achieve these?

- How can you discover your motivation(s)? And what implications do your motivations have for your wealth and portfolio?

Four motivations for sustainable investing

1. Positive outcomes: How can I use my money to drive positive outcomes?

Our world faces multiple ecological, social and economic challenges. For investors motivated by positive outcomes, these challenges represent opportunities to invest capital in companies and/or projects with commercial solutions to these issues.

In this case, you likely feel a responsibility to make the world a better place. Or there may be a specific issue that you, your family, or organisation may want to help solve. Additionally, you may want to invest for positive outcomes to add another tool to your philanthropic efforts.

Your investment strategy centres on using your wealth to catalyse change and contribute to solutions. For example, empowering villages’ clean energy infrastructure or improving life outcomes for young people by creating pathways into employment, education, or training.

Your expectations around the financial returns may vary depending on the investment opportunity. Sometimes you will seek a market-rate return for putting your capital at risk. Sometimes the potential impact will be more important than any potential financial gains. Ultimately though, you will make a choice about the priorities before investing.

Overall, this approach allows you to use your wealth to influence the people and the planet.

2. Values alignment: How do I invest in things that align with my values?

Our values guide our views of right and wrong and how we behave. For the values-aligned investor, these same principles should extend to how you invest. They can also ensure your family’s identity and ethics are reflected in your portfolio.

As a values-aligned investor, you would avoid sectors or companies that contradict your ethical views or would cause embarrassment if publicly known. You may also want to use your investments to signal what matters to you. Most importantly, you want to avoid your investments from causing what you believe would be harmful.

These values can stem from religious doctrine, personal experiences, or broader social norms. Families or organisations may also have expressed a set of values. In both, the principle remains the same, investing in a way that matters to specifically to you.

This feeling is often visceral in that you wouldn’t want to profit from activities that would make you feel uncomfortable or embarrassed. For example, if health and well-being is a core value, you’d likely avoid companies whose products have negative health outcomes, such as food companies, lifestyle products, or tobacco companies.

This approach brings piece of mind, knowing your portfolio aligns with what you, your family, or organisation believes.

3. Financial Returns: How do I capitalise on the sustainability movement to maximise my financial returns?

Sustainability challenges create both financially material risks and opportunities for companies – and consequently for investors. Taking sustainability factors into account therefore can be seen as prudent portfolio management.

For investors motivated primarily by financial returns, sustainability issues matter chiefly for their economic consequences, rather than issues themselves. You may seek to derisk your portfolio from sustainability challenges that may have a financial impact, or to profit from growth in sectors or companies that are commercially addressing social and environmental challenges.

This pragmatic view means a portfolio might simultaneously hold companies with opposing impacts on the world. For example, investing into traditional oil and gas companies as well as renewable energy companies if both present compelling return potential. If there are positive outcomes generated from your investments, these will be nice to know, but not meaningful to you to seek out.

This approach adds sustainability into the investment process through a financial materiality lens to serve your financial interests.

4. Family Engagement / Legacy: How do I use my investments to help the family to stay together?

Creating and maintaining wealth across generations requires more than creating financial returns. It demands learning how to be effective stewards of wealth. Sustainable investing can create a bridge connecting generations for both resilience and renewal of wealth and family.

If family engagement motivates your investing, you’re focused on transitioning family financial wealth successfully. This also helps to improve the probability that wealth generated previously will be protected and grown for future generations. As well, the opportunity to perpetuate or improve your family reputation and name.

This motivation often arises as current family heads worry about the family fragmenting after their death. While legacy becomes increasingly important to the older generations, younger ones also play a crucial role in shaping it. By actively involving the next generation(s), you demonstrate their value to the family and ensure their beliefs, values, and investment considerations are included.

Sometimes this requires adapting the family business to the changing industry or geopolitical dynamics. Or even finding alternative paths to wealth creation. For example, families with interests in hard-to-abate, high carbon emissions sectors, such as cement, shipping, real estate, or steel, may look to invest in decarbonisation technologies.

This approach focuses on family continuity, seeking to bring, and benefit, from the family staying together.

The value in understanding your motivations and those of others

Motivations are neither static nor exclusive. You may hold multiple drivers simultaneously, and family members likely will differ in their priorities. Personal background, values, milieu, and financial circumstances all influence the key motivations around sustainable investing. (We explore this further in Article 3 around social norms and family dynamics.)

Investors with different motivations may select identical investments. For example, a positive outcome investor and a financial returns seeker may both choose to invest in a solar farm, albeit for different reasons. In general, while younger generations tend to integrate financial and impact considerations more naturally, sustainable investing transcends age boundaries.

This dynamic plays out frequently within the families of many alumni. Parents may not prioritise impact or financial returns, but frequently they care about legacy and family cohesion. In these cases, they will embrace sustainable investing when shown it can help bridge generational divides.

Motivations also evolve across generations. A family that created wealth through fossil fuels may initially view the benefits in terms economic growth and job creation. Younger generations though may see “greening” the family business as both financially prudent and environmentally imperative.

Understanding what may drive you or others to undertake sustainable investing offers several advantages:

1. Intentional focus: Clear motivations sharpen your investment approach, helping you select opportunities that genuinely serve your goals.

2. Portfolio construction: Knowing your core drivers can help shape the right asset allocation and selection of investments for your portfolio.

3. Family cohesion: Just as families bond through meals, prayer or shared activities, investing with purpose can unite generations, build legacy and ensure wealth continuity.

4. Navigation of family dynamics: A family portfolio that accounts each member’s motivations helps to mediate conflicts, strengthen relationships, and facilitate succession planning.

Overall, sustainable investing represents an ongoing commitment to align investment strategies with the aspects that matter most to wealth holders. By understanding your motivations, you can create an investment approach that has the potential to generate financial returns and align with your deeper purpose.

Voices of experience

Over ten years, CSP has trained more than 240 participants in the Impact Investing for Next Generation programme. Fostering a deeper understanding of these motivations has helped investors enhance both the effectiveness and impact of their strategies, paving the way for meaningful, lasting change.

To bring these motivations to life, we interviewed CSP alumni Sam Oliver and Sheng Yang Er, who shared their personal journeys in sustainable investing.

Sam Oliver’s perspective:

Sam Oliver is a Scottish tech entrepreneur, property investor, and author who launched his first startup at just 20 years old. He’s known for building Lead.Pro, a marketing start-up sold to private equity in a multi-million-pound cash deal. His latest venture, Open-Fi, provides WhatsApp AI Sales Agents to increase web traffic conversion. Sam’s leadership experiences include serving as a board advisor to Nutri AI, a health tech startup, and The Turing Trust, a charity providing technology to schools in sub-Saharan Africa.

Primary motivations: Positive outcomes, Values alignment.

In my early days, investing felt like a purely financial endeavour, a naive separation from the broader impact of wealth. Through my journey with the CSP programme, I discovered a profound opportunity to drive systemic change while achieving solid financial returns. This realisation came through a commitment to rigorous education on both fund and direct deal due diligence.

My Quaker background, steeped in values of Peace, Truth, Equality, and Simplicity, shaped my ethical approach to investing. Yet, as a fifth-generation member of a family business, I struggled with the complexities of wealth, often viewing financial discussions through a lens of shame. Still, this unique background fuels my pursuit of meaningful, ethical business ventures.

As I reflect on our fleeting existence, I find joy in the idea of leaving the world better than I found it. This principle drives me to harness my resources for future generations, focusing on long-term systems change. While I don’t have all the answers, I strive toward this noble goal.

My motivations have evolved, now centring on biodiversity and environmental issues. I believe that improving land management practices can yield significant benefits, intertwining my ambitions with broader goals like income equality and education – key Sustainable Development Goals (SDGs). With limited time, it's vital to choose focus areas that resonate deeply for sustained impact.

Sheng Yang Er’s perspective:

Sheng Yang is a private investor based in Singapore, deploying impact capital towards earlier stage opportunities primarily in the decarbonisation space. He is a key donor and supporter of the CSP, as well as an alumnus of the Next Gen Impact Investing programme co-initiated at the Initiative for Responsible Investment at Harvard University and the University of Zurich. He previously worked for four years as an investment analyst at a top European credit manager on its European Syndicated Loans and High Yield team. He is also a member of Toniic.

Primary motivations: Financial returns, Positive outcomes, Family engagement and Legacy

As I reflect on my journey towards sustainable investing, it becomes clear how deeply my motivations shape my strategy. My commitment to addressing climate change has led me to hone in on my passion for environmental stewardship. This clarity allows me to prioritise investments that promise not only substantial returns, but also genuine impact, avoiding those that simply offer a feel-good factor.

Growing up, my family's strong values emphasised responsibility toward the planet. Dinner table discussions often centred on our duty to future generations, which naturally aligned with my desire to make meaningful investment choices today. This cultural foundation reinforces my commitment to impact investing.

Identifying my motivations was straightforward. I’ve always cared deeply about climate change and had a professional interest in finance. The pivotal moment came during the Next Gen CSP Impact Investing programme, where I discovered the intersection of these passions.

Impact investing became my pathway to merge my financial career with my commitment to sustainability. Through introspection, I identified my primary motivation: maximising the effectiveness of my investments to combat climate change. While ethical considerations are important, they take a backseat to my goal of achieving measurable impact. This focus drives my approach to sustainable investing, ensuring that my efforts contribute to meaningful change.

Acknowledgments:

Sam Oliver, Founder at OpenFI, technology entrepreneur, author and investor

Sheng Yang Eer, CIO at A-IT Software Services, entrepreneur and investor

Reflection questions: Identifying your motivations

Understanding your motivations is key to effective sustainable investment decisions. As well, knowing them will help you to navigate the obstacles we’ll discuss in Article 3 and to influence others, as we’ll discuss in Article 4.

Start by considering these reflection questions:

- What is the purpose of your financial wealth?

- What do you want your investments to achieve?

- What matters most to you? Your family? Or your organisation?

- What are you unwilling to compromise on?

Read the summaries below and see which of the four motivations resonate the most. Reflect on your experiences to identify which drivers best explain your decisions. Try allocating 100 points across the motivations to determine which are primary, secondary, or absent.

- Values alignment: For what I believe in, I am willing to forgo financial returns. I don’t want to profit in companies that don’t reflect our values.

- Positive outcome: I am disturbed global challenges and believe I have a responsibility to use my wealth for social and environmental impact. The opportunity to catalyse change motivates my investing.

- Financial benefits: Adding a sustainability lens is primarily for financial performance. Because sustainability creates both risks and opportunities, I want my portfolio to be managed accordingly.

- Family engagement and legacy: My priority is family cohesion and sustainable investing can provide a bridge for successful intergenerational wealth transfer. It can also enhance our family legacy while keeping the family together.

Barclays Private Bank disclaimer

This communication is general in nature and provided for information/educational purposes only. It does not take into account any specific investment objectives, the financial situation or particular needs of any particular person. It not intended for distribution, publication, or use in any jurisdiction where such distribution, publication, or use would be unlawful, nor is it aimed at any person or entity to whom it would be unlawful for them to access.

This communication has been prepared by Barclays Private Bank (Barclays) and references to Barclays includes any entity within the Barclays group of companies.

This communication:

(i) is not research nor a product of the Barclays Research department. Any views expressed in these materials may differ from those of the Barclays Research department. All opinions and estimates are given as of the date of the materials and are subject to change. Barclays is not obliged to inform recipients of these materials of any change to such opinions or estimates;

(ii) is not an offer, an invitation or a recommendation to enter into any product or service and does not constitute a solicitation to buy or sell securities, investment advice or a personal recommendation;

(iii) is confidential and no part may be reproduced, distributed or transmitted without the prior written permission of Barclays; and

(iv) has not been reviewed or approved by any regulatory authority.

Any past or simulated past performance including back-testing, modelling or scenario analysis, or future projections contained in this communication is no indication as to future performance. No representation is made as to the accuracy of the assumptions made in this communication, or completeness of, any modelling, scenario analysis or back-testing. The value of any investment may also fluctuate as a result of market changes.

Where information in this communication has been obtained from third party sources, we believe those sources to be reliable but we do not guarantee the information’s accuracy and you should note that it may be incomplete or condensed.

Neither Barclays nor any of its directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses (in contract, tort or otherwise) arising from the use of this communication or its contents or reliance on the information contained herein, except to the extent this would be prohibited by law or regulation.

Barclays offers private and overseas banking, credit and investment solutions to its clients through Barclays Bank PLC and its subsidiary companies. Barclays Bank PLC is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority (Financial Services Register No. 122702) and is a member of the London Stock Exchange and Aquis. Registered in England. Registered No. 1026167. Registered Office: 1 Churchill Place, London E14 5HP.

Barclays Bank PLC, Jersey Branch has its principal business address in Jersey at 13 Library Place, St Helier, Jersey and is regulated by the Jersey Financial Services Commission. Barclays Bank PLC, Isle of Man Branch has its principal business address in the Isle of Man at Barclays House, Victoria Street, Douglas, Isle of Man and is licensed by the Isle of Man Financial Services Authority. Barclays Bank PLC, Guernsey Branch has its principal place of business at St Julian’s Court, St Julian’s Avenue, St Peter Port, Guernsey and is licensed by the Guernsey Financial Services Commission under the Banking Supervision (Bailiwick of Guernsey) Law 1994, as amended, and the Protection of Investors (Bailiwick of Guernsey) Law 1987, as amended.

Barclays Bank Ireland PLC, trading as Barclays and as Barclays Private Bank, is regulated by the Central Bank of Ireland. Registered in Ireland. Registered Office: One Molesworth Street, Dublin 2, Ireland, DO2 RF29. Registered Number: 396330. VAT Number: IE4524196D. Calls are recorded in line with our legal and regulatory obligations, and for quality and monitoring purposes.

Barclays Bank (Suisse) SA is a bank registered in Switzerland and regulated and supervised by the Swiss Financial Market Supervisory Authority FINMA. Registered No. CHE-106.002.386. Registered Office: Chemin de Grange-Canal 18-20, 1224 Chêne-Bougeries, Switzerland. Registered branch: Beethovenstrasse 19, 8002 Zurich, Switzerland. Registered VAT No. CHE-106.002.386. Barclays Bank (Suisse) SA is a subsidiary of Barclays Bank PLC.

In the Principality of Monaco, Barclays Bank PLC operates through a branch which is duly authorised and falls under the dual supervision of the Monegasque regulator ‘Commission de Contrôle des Activités Financières’ (with regards to investment services) and the French regulator ‘Autorité de Contrôle Prudentiel et de Résolution’ (in respect of banking and credit services, and prudential supervision). The registered office of Barclays Bank PLC Monaco branch is located at 31 avenue de La Costa, MC 98000 Monaco – Tel. + 377 93 15 35 35. Barclays Bank PLC Monaco branch is also registered with the Monaco Trade and Industry Registry under No. 68 S 01191. VAT No. FR 40 00002674 9.

Barclays Bank PLC (DIFC Branch) (Registered No. 0060) is regulated by the Dubai Financial Services Authority. Barclays Bank PLC (DIFC Branch) may only undertake the financial services activities that fall within the scope of its existing DFSA licence. Principal place of business: Private Bank, Dubai International Financial Centre, The Gate Village Building No. 10, Level 6, PO Box 506674, Dubai, UAE. This information has been distributed by Barclays Bank PLC (DIFC Branch). Certain products and services are only available to Professional Clients as defined by the DFSA.

Barclays Bank Plc (Incorporated in England and Wales) (Reg. No: 2018/599243/10) is an authorised financial services provider under the Financial Advisory and Intermediary Services Act (FSP 50570) in South Africa and a licensed representative office of a foreign bank under the Banks Act, 1990. Barclays Bank PLC, has its principal place of business in South Africa, at The Business Exchange, 140 West St, 4th Floor, Sandton 2057.

Barclays Bank PLC Singapore Branch is a licenced bank in Singapore and is regulated by the Monetary Authority of Singapore. Registered in Singapore. Registered No. S73FC2302A. Registered Office: 10 Marina Boulevard, #25-01, Marina Bay Financial Centre Tower 2, Singapore 018983.

Barclays Bank PLC, India branch (FCRN F01106) is regulated for its banking business and as authorised dealer by Reserve Bank of India and is registered with the Securities and Exchange Board of India as merchant banker and banker to an issue. Its principal place of business in India is at Level 32 and 33 (3301 A), Altimus, Worli Estate, Pandurang Budhkar Marg, Worli, Mumbai 400018, India. Transactions, products and services as offered from time to time are subject to the applicable laws and regulations of India.

You might also be interested in

Insights

Starting Your Family's Sustainable Investing Journey Part 4: How Do You Bring Others On The Journey?

The 3Cs framework: communication, connection, and commitment aims to help families find common ground and move forward together.

Insights

Starting Your Family's Sustainable Investing Journey Part 3: What Obstacles Will You Encounter?

Internal mindsets, family dynamics, and social norms are the real obstacles to sustainable investing. A guide on how to spot them.

Insights

Starting Your Family's Sustainable Investing Journey Part 2: Where Do You Want To Go?

Learn how to set clear ambitions and use the UN SDGs to define where you want your sustainable investing journey to go.